Staying Bulletproof: 5 Essential Compliance Rules for Every C-Corp

The primary reason entrepreneurs choose the C-Corporation structure is the unparalleled asset protection it provides. However, this protection is not a "set it and forget it" feature. It is a legal privilege maintained through rigorous compliance.

If you treat your C-Corp like a personal piggy bank or fail to document your decisions, a court can "pierce the corporate veil," making you personally liable for business debts. At LaNasa Global Solutions, we prioritize your protection.

Here are the five non-negotiable compliance pillars every C-Corp founder must master.

1. Formalize Your Corporate Bylaws

Your bylaws are the "Constitution" of your company. They dictate how the corporation will be governed, including how officers are elected, how shares are issued, and how disputes are resolved.

Why it matters: Without bylaws, you are subject to default state rules that may not align with your vision.

Action Step: Ensure your bylaws are drafted by professionals and stored in your corporate records book.

2. Hold (and Document) Annual Meetings

C-Corporations are legally required to hold at least one annual meeting for shareholders and one for the Board of Directors.

The "Minutes": You must record "Minutes"—a formal written record of what was discussed and decided.

Why it matters: In an audit or lawsuit, these minutes prove that the corporation is a separate, functioning legal entity.

3. Appoint and Maintain a Board of Directors

Even if you are the sole owner, a C-Corp must have a Board of Directors. The Board is responsible for high-level strategy and appointing the Officers (CEO, CFO, Secretary) who handle daily operations.

Modern Strategy: Many LGS clients use an Advisory Board to add "institutional weight" to their company, which is a major signal of credibility to lenders and government contractors.

4. Strict Separation of Finances

This is where most founders fail. Co-mingling funds using your corporate card for a personal lunch or vice versa is the fastest way to lose your legal protection.

The Rule: The Corporation’s money belongs to the Corporation. Personal compensation should only happen through a formal payroll (W-2) or documented dividends.

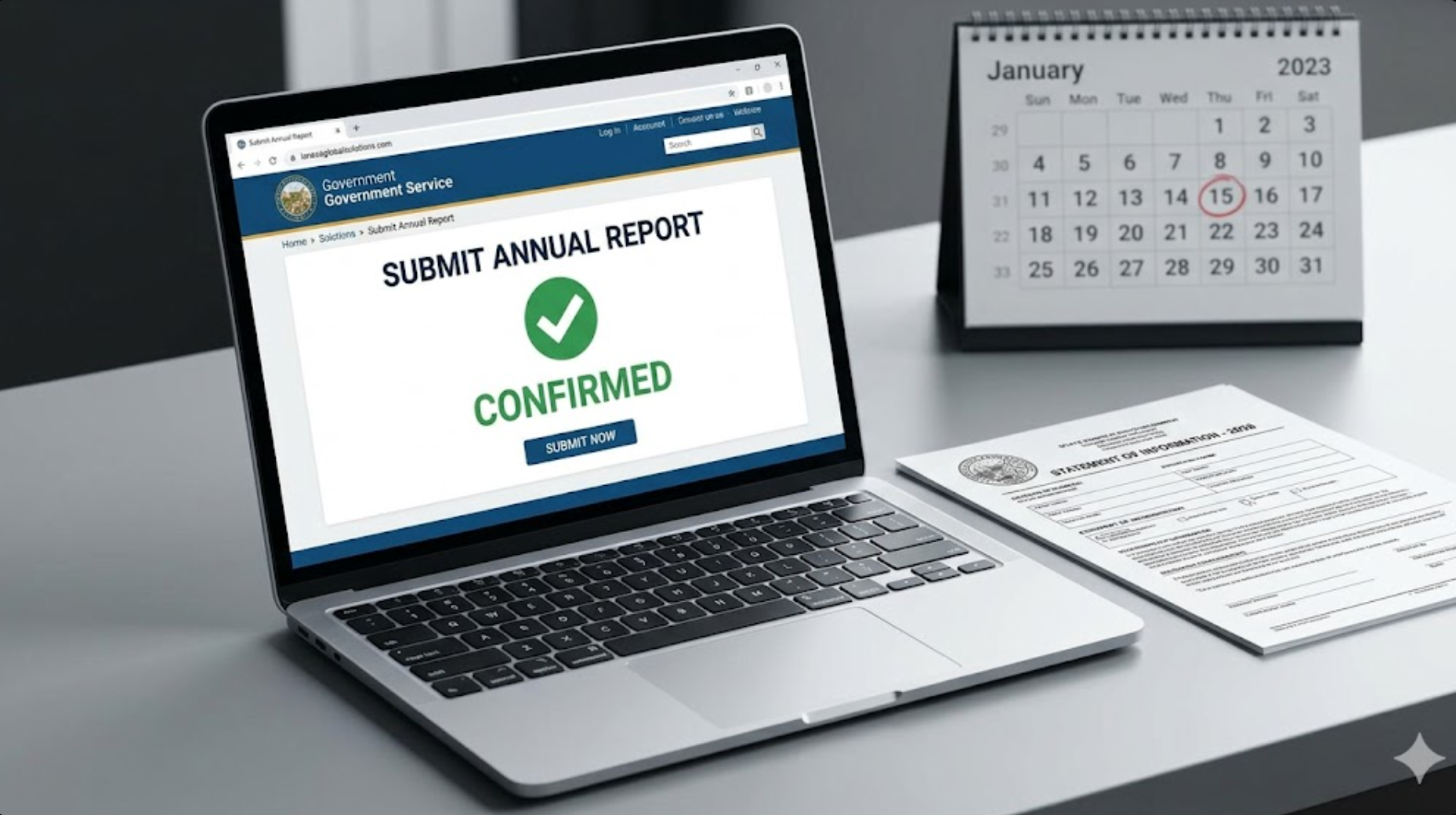

5. File Statement of Information & Annual Reports

Most states require C-Corps to file an annual or biennial report to keep the business in "Good Standing."

The Risk: Failing to file can lead to the administrative dissolution of your company, meaning you lose your "Inc." status and your tax benefits overnight.

The LGS Compliance Standard

Managing a C-Corp requires a higher level of discipline than a simple side hustle. But that discipline is exactly what allows you to scale to eight figures and beyond.

Is your C-Corp "Audit-Ready"?

Don't wait for a legal hurdle to find out your paperwork is missing. Our LGS Business Formation & Strategy team ensures your corporate records are airtight.

Download our Free Business Compliance Checklist